Janus Henderson: G7 yield curve echoing monetary slowdown signal

The assessment here that the global economy has entered a slowdown phase likely to last through late 2018 (at least) rests primarily on weaker monetary trends since mid-2017. The slope of the G7 yield curve – another longer leading indicator with a respectable historical record – is consistent with the monetary message.

23.04.2018 | 12:50 Uhr

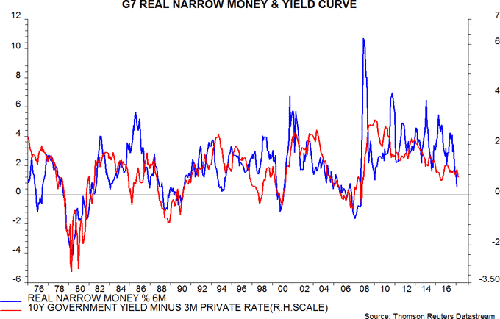

G7 six-month real narrow money growth has displayed a significant positive correlation historically with the slope of the yield curve, defined as a GDP-weighted average of 10-year government yields minus three-month money rates – see chart. The correlation is maximised by applying a two-month lag on real money growth, i.e. money growth appears to move slightly ahead of the yield curve.

G7 six-month real narrow money growth has displayed a significant positive correlation historically with the slope of the yield curve, defined as a GDP-weighted average of 10-year government yields minus three-month money rates – see chart. The correlation is maximised by applying a two-month lag on real money growth, i.e. money growth appears to move slightly ahead of the yield curve.

While the yield curve slope often gives a similar forecasting message to narrow money trends, the judgement here is that money signals are more reliable.

The yield curve has given some notable false signals historically, e.g. it inverted in 1986 and 1998 but no recession ensued over the following two years. Real narrow money trends did not suggest economic weakness on these occasions.

The yield curve, moreover, can be distorted by central bank efforts to control it through QE and forward guidance. Real narrow money growth picked up strongly between mid-2015 and mid-2016, correctly signalling global economic acceleration in late 2016 / 2017. The yield curve, by contrast, flattened over this period, possibly partly reflecting an increased G7 flow of QE following the start of the ECB’s programme in March 2015. The QE pick-up, indeed, may have both boosted money growth while distorting the yield curve signal.

A further consideration is that real narrow money appears to work better as a forecasting indicator than the yield curve slope in emerging economies. This may partly reflect financial market underdevelopment – the performance of the yield curve may improve as markets deepen and mature. A money-based global forecasting measure, therefore, is likely to outperform one based on interest rates.

Real narrow money trends and the yield curve slope are giving a similar message currently. The monetary slowdown has been accompanied by a flattening curve. Real money continues to grow and the curve has not inverted, so no recession signal has yet been given.

Diesen Beitrag teilen: