Schroders: Is Japan abandoning its cash conservatism?

Within global equities, one of the key themes we see emerging in 2015 is a shift in focus of corporate Japan from stockpiling to distributing excess cash; a trend which may awaken income-seekers’ interest in the country.

20.05.2015 | 15:09 Uhr

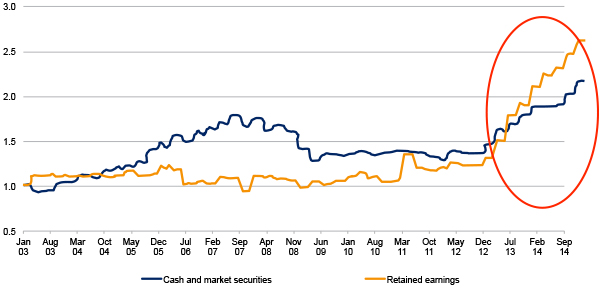

Japan has long been known as the “nation of savers” so it comes as no surprise that companies generally prefer to hold on to surplus cash rather than return it to shareholders. Corporate profits can be very volatile, given their high dependence on foreign demand, so management teams are often keen to preserve cash to provide a cushion in bad times. As a result, many companies hold more than 20% of their market capitalisation in cash - some even hold more than 50% - and shareholder returns on equity have significantly lagged that of other developed markets.

However, policymakers are keenly aware that the high corporate savings rate has been undermining growth and that stronger corporate governance is critical, both to boosting confidence in the market and to achieving economic growth targets. An improving global economy and the strong recovery in earnings that corporate Japan has experienced since Prime Minister Abe’s return to power at the end of 2012, means that companies are in a good position to let go of this cash conservatism and align their capital return policies more closely to those seen elsewhere in the developed world.

More chance of success this time around

Reform of the country’s corporate governance structure is encouraging greater interaction between management and shareholders, which gives the latter more of an opportunity to draw attention to inefficient balance sheets and effect change in capital distribution policies. This is certainly not the first time that Japan has attempted to tighten up its corporate governance. However, previous instances have largely stemmed from international pressure, whereas this time there is clearly a domestically-driven agenda with a much higher chance of real improvements as a result.

The introduction of a stewardship code and the creation in 2014 of the JPX-Nikkei Index 400 (Japan’s first broad index that includes only profitable companies with value-creating returns and good governance), have helped drive greater awareness of the benefits of proper governance. The index has performed well since its inception and the outlook for further strong performance is helped by the fact that the Government Pension Investment Fund (GPIF) has been moving equity mandate benchmarks to the JPX-Nikkei Index 400.

Clear signs of progress

This has sparked some dramatic changes in shareholder return policies already. For example, in order to make the cut for inclusion in the new index, Amada, a machine tool manufacturer, has committed to returning 100% of net profits to shareholders for the next two years.

Together, the introduction of the stewardship code and the creation of the JPX-Nikkei Index 400 are also resulting in a significant acceleration in the number of external directors on corporate boards. Japan’s Council of Experts, a group comprising both business and academic figures, has published the country’s first governance code, which is expected to come into effect in June. The code aims to provide a clear and significantly progressive set of rules intended to be enforced on a “comply or explain” basis.

Key feature of the stockmarket this year

Corporates are therefore facing rising pressure to return capital to shareholders and we are already seeing some clear signs of progress being made. We expect this increasingly to be a feature of the Japanese stockmarket. We also anticipate that greater scrutiny of inefficient balance sheets and more emphasis on capital return policies will drive a significant acceleration in dividend hikes and share buybacks this year.

Diesen Beitrag teilen: