Columbia Threadneedle: Recession, inflation, and interest rates cuts: what does it all mean for markets?

Exploring the factors that mean we’re arguing the case for a goldilocks scenario of growth, easing inflation and lower rates

20.09.2024 | 10:15 Uhr

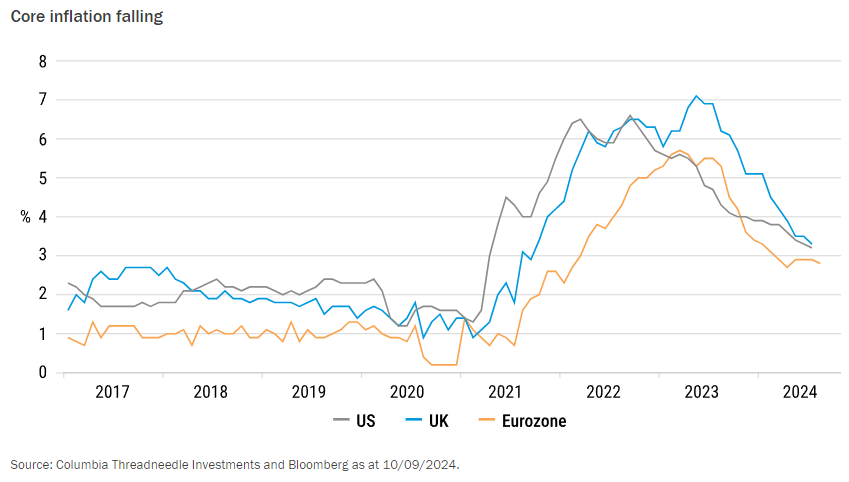

Investor fears over recession have had a spike in the US over the summer, with markets now discounting jumbo rate cuts by the Federal Reserve (Fed) by the end of the year. However, with inflation resuming its downward trend and economic growth resilient, we instead see that US ‘immaculate disinflation’ is back on course.

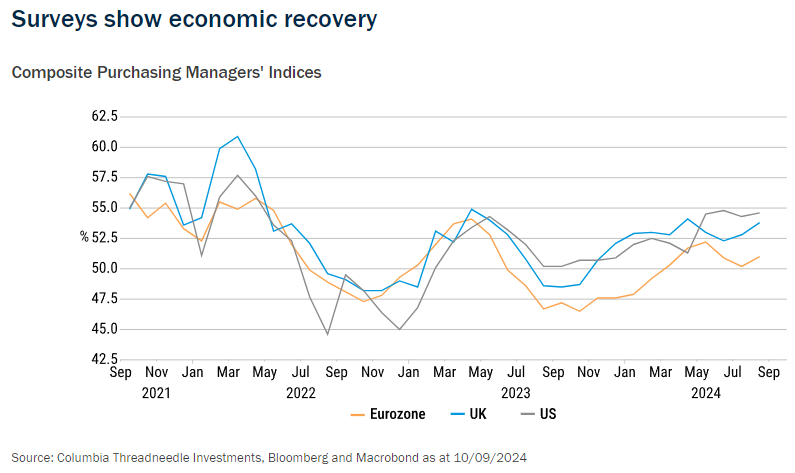

That same virtuous cycle, whereby lower headline inflation is lowering nominal wage growth and driving core inflation down, is a phenomena that we’re seeing in all developed economies and that’s positive for the consumer and for central banks. Economic recovery is clearly accelerating in the UK, which reduces the scale of coming interest rate cuts. Meanwhile Europe is lagging, with structural changes hindering German growth, so the European Central Bank (ECB) has taken the lead with interest rate cuts.

Continued economic growth, falling inflation and the prospect of lower interest rates make both bonds and equities attractive. But we are not quite as optimistic on equities, as there’s a lot already priced in.

US ‘immaculate disinflation’ back on course

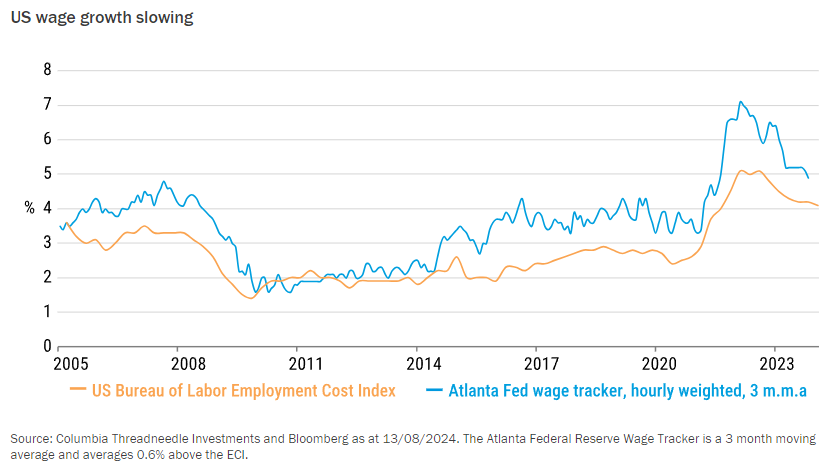

Recession fears in the US increased as a rise in unemployment triggered the Sahm rule. That rule has always worked – never predicting a recession that didn’t happen or failing to predict one that did happen – so it’s been a darn good rule. However, I don’t think it’s going to work this time. The inventor of the rule, Claudia Sahm, also doesn’t think that it’s going to mean a recession. Instead, the uptick in unemployment has eased the labour market and allowed wages to follow inflation down.

We see slowing but continued expansion of the US economy. A key driver has been consumer expenditure, however, having spent down their savings, the US consumer will have to moderate their spending in line with, and indeed below, income growth. The big boost to US manufacturing and investment from government programmes will also tail off. For both of those reasons the US economy is set to slow. On the other hand, interest rates are set to come down, so there are other, positive factors.

No recession would remove a major risk for the equity market, but it also means a risk of disappointment in the bond market, as expectations are now back up to a 1% cut in US interest rates by the end of the year. That seems unlikely as growth continues and wage inflation is still easing down from relatively high levels.

The US election outcome is too close to call. We have two Presidential candidates that are further apart in policies and philosophies than any that I can remember. Trump’s policies of tax cuts, tariff increases, and deregulation would be equity market friendly, but bad for bonds as tariffs would raise inflation. Much depends on which side wins Congress – if Republicans win the Senate and retain the House, barriers to radical change for a Trump presidency would be limited.

UK to see good growth and low inflation for now; major challenges for new government

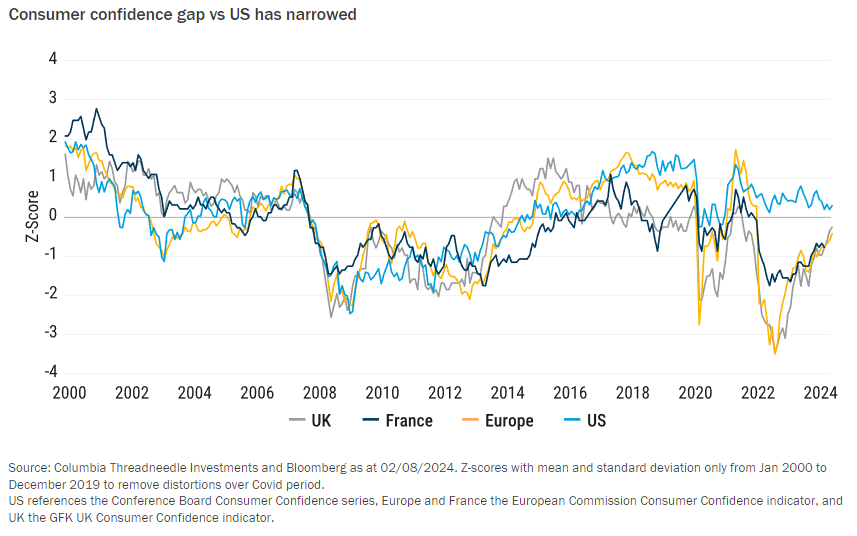

UK is now forecast to be the fastest growing economy in the G10 – beating the US by the last quarter of the year. In contrast to the US, consumers in the UK have been saving a higher proportion of income, even as real incomes were squeezed. That reflected record low consumer confidence due to the energy crisis precipitated by the invasion of Ukraine. As that uncertainty declines and as real incomes recover, there is scope for consumer spending to rise further as those precautionary savings decline back to normal levels. The key housing market has already switched from mild declines to mild increases – which provides a boost to transactions and so a significant stimulus to economic growth.

While UK inflation peaked later, it has now fallen back to target, but the Bank of England is likely to cut rates at a slower pace, focused on wage inflation, which has fallen significantly but remains too high, rather than growth, which is robust. Headline inflation will rise modestly from currently levels due to higher energy costs, but sterling strength this year will act to reduce inflation over the coming 12 months.

The new government has a radical agenda but is constrained by significant challenges including government debt close to 100% of GDP and productivity that has lagged since the 2008 crisis. Labour is going to end up taxing more, spending more and borrowing more, but only modestly.

European growth to recover slowly in 2024

European growth rates remain steady, but anaemic. Germany is the main drag, due to structural problems in the important car industry and from the end of cheap natural gas from Russia, though there are signs that the negative impact is bottoming. There will be a slight fiscal squeeze from EU rules next year.

Europe is also seeing the virtuous cycle whereby lower headline inflation is tempering nominal wage growth and driving core inflation down. This has allowed the ECB to take the lead in cutting interest rates to support economic growth. As real incomes recover, there is scope for consumer spending to rise further as precautionary savings levels decline back to normal levels.

Lower interest rates make bonds and equities attractive….but there’s a lot priced in

The goldilocks scenario that I’ve set up – continued growth, falling inflation and interest rates – is positive for bonds and equities.

We are positive on government bonds given the attractive yields. Our overweight has been reduced as yields have fallen back from their highs.

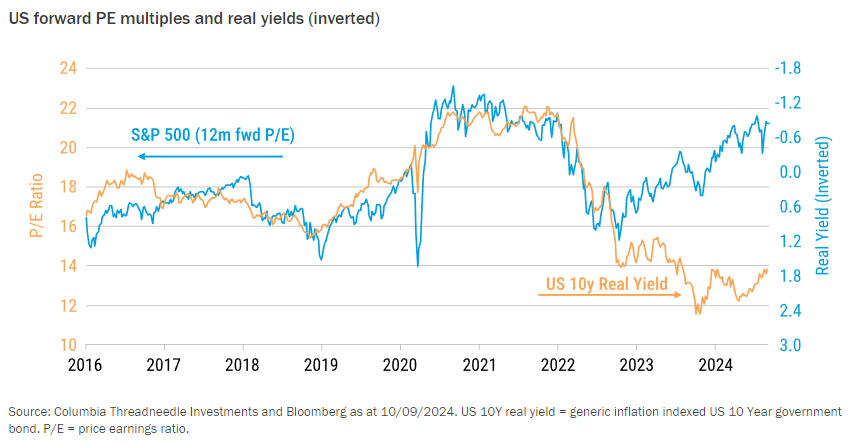

Equity valuations are stretched, specifically in the US. However expensive equities were not a reason to sell, as equities have only become more expensive this year. Instead, the risk comes from when we get a recession, then expensive equities fall further. But I don’t think we’re going to get a recession in any realistic period for forecasting. We’re still positive on equities, though the valuation risk does make us a bit less optimistic.

We switched our overweight in equities from Japan to Europe on the basis of earnings outlook – also reflecting that people have become more optimistic about Japan, but overly pessimistic about Europe.

Gold has also diverged from a measure of value. That divergence started when Putin invaded Ukraine and Euro and US dollar assets were frozen for over 2,000 groups and individuals. It has moved further as some element of those frozen assets has been diverted to rebuild Ukraine. That represents a significant shift in the safe haven status of these assets – to the benefit of gold.

Equity valuations decouple from real yields

Diesen Beitrag teilen: