Schroders: Do rising rates reduce returns on income assets?

Our research, which looks at episodes of rising rates since 1970, suggests income-producing assets don’t perform as investors might expect.

18.09.2017 | 10:59 Uhr

Many will remember to their cost the infamous “taper tantrum” in June 2013. It was the moment Ben Bernanke, the then Chairman of the US Federal Reserve, indicated that the quantitative easing (QE) would be scaled back, or tapered.

The QE programme had fed money into the financial system to stimulate the economy following the financial crisis of 2008. It had helped keep the yields on government bonds at exceptional lows.

In a matter of hours, government bond yields jumped by over a percent as bond holders unloaded assets. It was perhaps one of the more painful illustrations of the inverse relationship between government bond yields and prices (as yields increase, prices fall).

Many assume that the same relationship holds true for all income-generating assets - that when rates and yields rise, prices will fall.

It may therefore come as a surprise that our research suggests this is, in many cases, a fallacy. Indeed, even in 2013, very few income asset returns suffered any lasting damage, and many actually recorded positive returns by the end of the year.

When we talk about income assets we mean a universe that extends well beyond government bonds to include the likes of investment-grade bonds (issued by more creditworthy companies), high-yield bonds (issued by less creditworthy companies, but offering more income in exchange), real estate investment trusts (REITs, a type of property company), emerging market bonds and high-dividend equities (which offer above average income).

They are particularly relevant today because, while these assets have all performed strongly over the past few decades, boosted by low government bond yields, the climate is definitely changing. The US Federal Reserve now seems determined to raise interest rates. Several rate-setters on the Bank of England’s Monetary Policy Committee recently voted for a rise and questions are being raised about whether the European Central Bank will follow suit. In light of all that, many investors could be forgiven for wondering whether the party is over and it is time to sell these income assets.

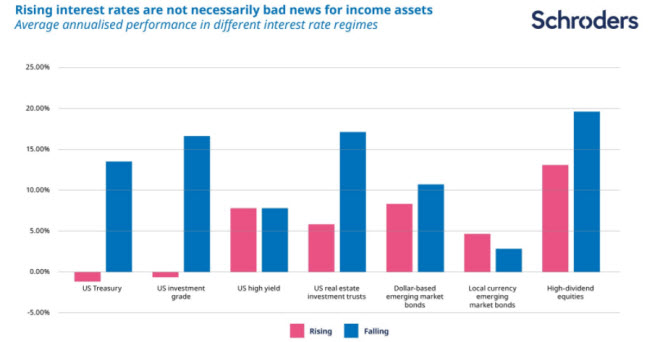

We have looked into past episodes of rising rates in the period since 1970 and concluded that they do not necessarily spell doom for such assets. In fact:

All income assets produced positive returns, on average, in rising-rate environments, with the exception of government and corporate bonds.

Government bonds (such as US Treasuries) and investment-grade corporate bonds have performed far worse when yields have been rising than when they have been falling.

Many other assets typically included in income portfolios have held up well, and some have actually performed better, when yields have been rising.

Asset classes have varying lengths of historical data. Source: Bank of America Merrill Lynch (BAML), Datastream, FRED, Keneth French, JP Morgan (JPM), MSCI and Schroders, as at 28 February 2017. Past performance is not a guide to future performance and may not be repeated.

These conclusions should provide comfort for income investors. As interest rates tend to rise in anticipation of stronger economic growth, assets which are more sensitive to economic growth (such as high yield debt, REITs and high-dividend equities) can still perform well. As corporate fundamentals usually also improve, this provides a boost to corporate earnings and improves the creditworthiness of borrowers, supporting equities and corporate bonds.

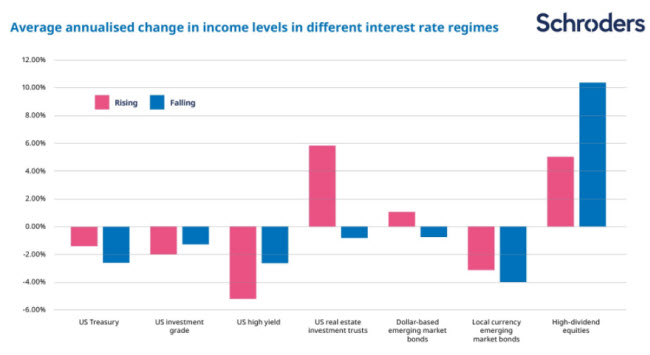

Moreover, our analysis confirms the general assumption that income levels are generally less sensitive to changes in interest rates than overall returns. Companies are loath to cut dividends, given the negative signal that it sends to the market, while coupons on bonds are one of the first claims on a company’s income, ranking above other demands. With few exceptions, we found the impact of rising interest rates on income levels has been minimal and in some cases income levels actually picked up when yields rose. In fact, income levels overall deteriorated more during times of falling interest rate environments than rising.

Asset classes have varying lenths of historical data. The coupon yields of all bond assets have been adjusted for market price, with the exception of local EMD, where market price data were not available. Source: Datastream, BAML, FRED, Kenneth French, JPM, MSCI and Schroders, as at 28 February 2017. Past performance is not a guide to future performance and may not be repeated.

In all this it is important to remember that, like any other asset class, investing in income assets requires an adequate time horizon. Being patient in income investing and not panicking when interest rates go up is a sound strategy. We found that, more often than not, patience paid off for both returns and the income generated by the asset.

The variation in performance of income assets, combined with the fact that most returns have been positive during rising-yield environments, underlines the importance of asset allocation during times of rising rates. Indeed, we would argue that, if investors can combine savvy asset allocation with an awareness of income assets’ behaviour when rates rise, they should add value even when the going looks tough and the temptation might otherwise be to sell.

Important information

Please remember that past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of any overseas investments to rise or fall. High yield bonds (normally lower rated or unrated) generally carry greater market, credit and liquidity risk. Emerging markets generally carry greater political, legal, counterparty and operational risk. Funds that invest in real estate related securities and investments focus on specific sectors and can carry more risk than funds spread across a number of different industry sectors.

Die hierin geäußerten Ansichten und Meinungen stellen nicht notwendigerweise die in anderen Mitteilungen, Strategien oder Fonds von Schroders oder anderen Marktteilnehmern ausgedrückten oder aufgeführten Ansichten dar.

Der Beitrag wurde am 14.09.17 auch auf schroders.com veröffentlicht.

Diesen Beitrag teilen: