Henderson: Eurozone money signal still positive

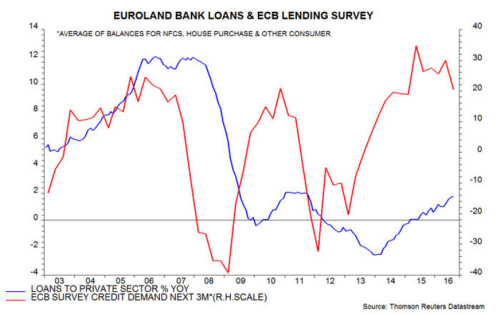

Annual growth of bank loans to the private sector remains weak, at 1.7% in August, but is trending gradually higher, with the ECB’s bank loan officer survey signalling rising credit demand.

28.09.2016 | 09:51 Uhr

The consensus forecast is for Eurozone GDP growth to slow from 1.5% in 2016 to 1.2% in 2017. Monetary trends suggest that this is too downbeat and GDP will continue to rise at a 1.5-1.75% annual rate – it increased by 1.6% in the year to the second quarter. Such growth would be comfortably above trend economic expansion estimated by international forecasting bodies at about 1% per annum, implying a continued decline in unemployment and – probably – firmer “core” inflation.

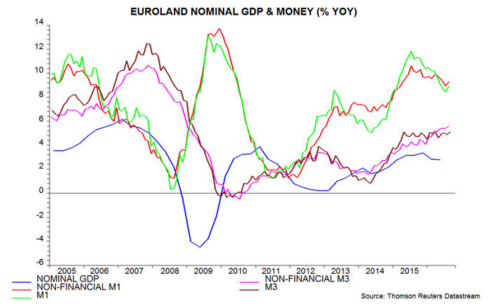

Some commentary before today’s release of August data expressed concern about a cooling of monetary trends. Annual growth of narrow money M1 was 8.4% in July, well down from a peak of 11.8% in July 2015, with M3 expansion easing to 4.8%, a three-month low. The August numbers were better, showing annual growth of 8.9% and 5.1% respectively.

The earlier concern was not shared here, on the grounds that the headline M1 / M3 numbers were being pulled down by a decline in growth of financial institutions’ deposits, which contain little information about near-term economic prospects. Annual growth of non-financial M1 – comprising holdings of households and non-financial corporations – was 8.9% in July, increasing to 9.3% in August. Non-financial M3 expansion rose to 5.6% last month, the fastest since 2008 – see first chart.

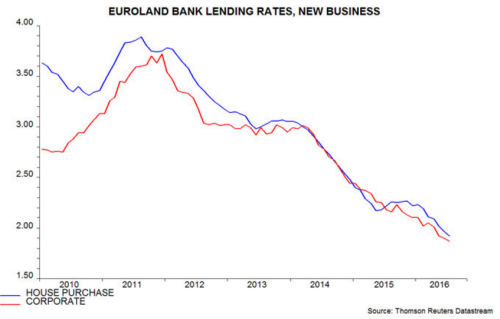

A further reason for remaining sanguine was / is that earlier policy easing has yet to have its full impact on monetary conditions. Interest rates on new bank loans, for example, are still declining, with potential positive effects on credit demand and monetary expansion – second chart.

Annual growth of bank loans to the private sector remains weak, at 1.7% in August, but is trending gradually higher, with the ECB’s bank loan officer survey signalling rising credit demand – third chart.

Solid monetary growth since 2013 has lifted domestically-generated inflation – as measured by the annual change in the GDP deflator – to 1.1% as of the second quarter, as well as delivering respectable economic expansion. Nominal GDP rose by 2.8% in the year to the second quarter, outpacing increases of 2.4% in the US and 1.5% in Japan, though below a 2.9% UK gain. Eurozone deflation risk was and remains low.

Die Wertentwicklung in der Vergangenheit ist kein zuverlässiger Indikator für die künftige Wertentwicklung. Alle Performance-Angaben beinhalten Erträge und Kapitalgewinne bzw. -verluste, aber keine wiederkehrenden Gebühren oder sonstigen Ausgaben des Fonds.

Die Informationen in diesem Artikel stellen keine Anlageberatung dar.

Diesen Beitrag teilen: