NN IP: Value rebounds in style reversal

In June we saw a style rotation from growth to value as a result of higher bond yields, better macro data and a rebound in oil and commodity prices. We see an increased likelihood that this trend will continue. Despite the recent correction, we keep our positive view on IT.

06.07.2017 | 16:26 Uhr

Value rebound

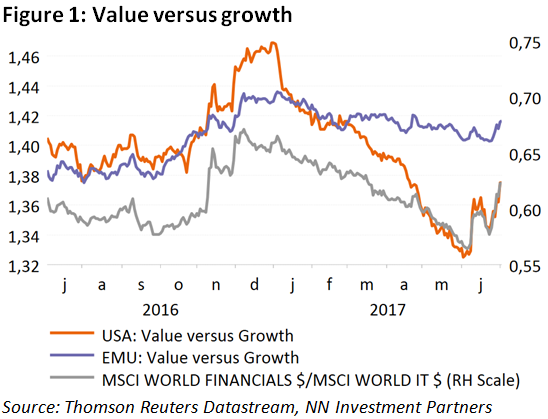

The past month looked very different from the previous ones as we witnessed a sudden reversal from growth towards value. Especially in the US the rotation was sharp, which can be explained by the bigger weight of the technology sector in the US (22%) versus the Eurozone (7%). The parallel of the value/growth performance in the US with the financials/technology performance is striking in this respect, as can be seen in Figure 1.

So what has changed? We see three important top-down drivers. The main catalyst is undoubtedly the sharp rise in treasury yields following the perception of a hawkish shift at the ECB, BoE and the Fed. We think the market has gotten ahead of itself given the absence of (wage) inflation. We have not changed our policy path for the ECB or the Fed. However, we may see further episodes like this as we are in unconventional monetary policy territory, lacking anchor points.

The second factor is the broad pick-up in macro-economic data. The US Manufacturing PMI, the Japanese Tankan and also emerging market data continue to point towards a further improvement in economic momentum. The data did also beat expectations, ending a three-month decline in the Citigroup economic surprise index.

The third element is the upturn in commodity prices, and oil in particular. The oil price is not only of importance for the profitability of the energy and materials sectors, but also crucial for the capex outlook. Energy prices also influence inflation expectations, which can feed through into monetary policy (expectations) which brings us back to the first point on bond yields.

Sector rotation

When these three factors occur simultaneously, this means good news for financials, commodity cyclicals and end-user cyclicals. Financials benefit through more support for the interest rate margin, higher credit growth and lower provisioning for bad loans. The cyclical sectors benefit from the improvement in the macro outlook, driving their top-line growth and margin developments.

The flipside is for the sectors that have previously benefitted from the search for yield theme, like utilities, real estate and telecom. Also the non-cyclical stable growers like consumer staples and health care face headwinds under this scenario as investors shift their portfolios.

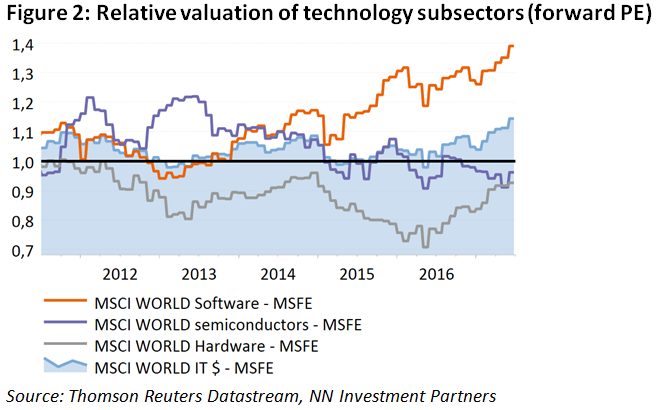

Within this framework, the technology sector is a somewhat different story. Technology has corrected around 6% (in euro) over the past three weeks. Together with health care it is considered as a growth sector by “definition” and, as such, both have suffered from the switch from growth into value. In addition, being overweight technology was a crowded trade. However, there is an important cyclical component in the IT sector, especially through the semiconductor and hardware segments. This distinguishes it from the health care sector.

We keep a medium overweight in technology, based on its strong earnings momentum and reasonable valuation. As such it is by no means comparable to the situation that prevailed at the end of the nineties, when there were no profits and unrealistic growth expectations build into valuations. Although the IT sector trades at a 14% premium, splitting it up in its main subindustries reveals that only the software segment trades at a significant 40% premium to the overall market. Semiconductors and hardware even trade at a small discount. It is also a sector than can perform well in a low-growth environment. Of course, due to sometimes overly dominant market positioning, regulation could become a fundamental headwind.

Going forward, whether or not this value rotation will continue will depend on the interaction between macro data, bond yields and the behaviour of central banks. We believe there is currently a higher likelihood that this will continue than a couple of weeks ago, given the macro environment and our view of gradually higher interest rates. We also close the underweight in materials.

Diesen Beitrag teilen: