Morgan Stanley IM: Growing Up and Out - The Impact of Aging Populations on Housing

While the fundamentals and investment thesis for senior housing are compelling, the subtleties of different care segments and the service-oriented nature of caring for elderly residents create operational risk, requiring a nuanced investment strategy and dedicated operating expertise.

21.06.2024 | 06:03 Uhr

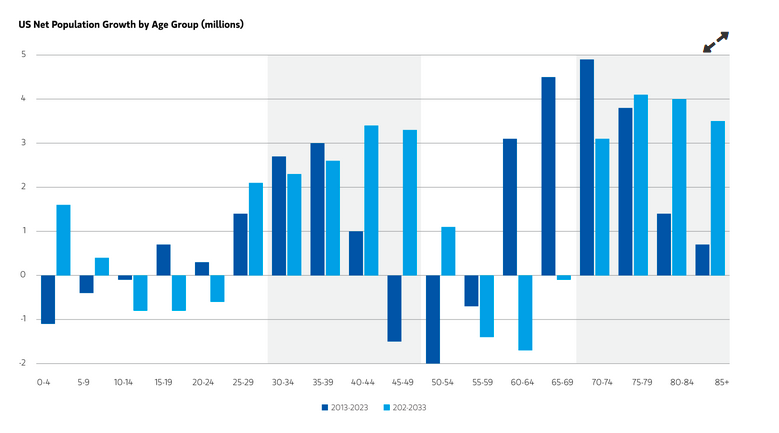

- Over the next 10 years, population growth will shift to the 70+ and 30- 50 age groups, potentially creating attractive residential opportunities tailored to a unique set of living preferences.

- A wide affordability gap between the cost of owning and renting, exacerbated by a lack of affordable supply, is creating a favorable demand/supply balance for single-family rental owners.

- Senior housing affordability has improved by more than 10 percentage points over the past decade, supporting occupancy gains and rental growth momentum.

As the U.S. population braces for major demographic shifts, the residential real estate landscape is evolving quickly alongside its industrial counterpart. Aging populations are transforming residential housing demand as dramatically as the overhaul of the global supply chain is changing industrial real estate. The two largest age groups in the U.S. -- millennials (72 million) and baby boomers (69 million) -- desire vastly different living preferences. Over the next 10 years, the 30-50 and 70+ age groups will lead population growth.1 Millennials are aging out of apartments and seeking larger homes more suited to families. By 2033, nearly all baby boomers will be 70 or older, bolstering demand for housing with increased care options, such as assisted living and nursing facilities.2

These preference changes are creating strong demand tailwinds for single-family rental housing (given the affordability challenges of buying a home) and senior living facilities.

Single-family Rental Trends

The outsized growth and aging within the 30- to 50-year-old group

is fueling demand for single-family homes. Societal shifts have delayed

this group reaching adult milestones such as getting married, having

children and owning a home. For example, the percentage of married

30-year-olds has dropped from 67% to 47% over the last 20 years, while

the percentage of people having children by age 30 has sunk from 53% to

35%, and the percentage of homeowners has plunged from 43% to 33%3.

These delayed life decisions have supported robust demand for

multifamily housing over the past decade. However, as this group

continues to age, get married and have children, their preference for

single family housing is expected to rise. At the same time, they are

faced with a widening affordability gap between the cost of owning

versus renting, due to rapidly rising house prices (up ~50% over the

last five years4), elevated mortgage rates (up 4 per cent

since 2022), a lack of affordable housing supply, and inadequate savings

to fund downpayments. These trends should continue to propel demand for

single-family rental housing, which is still under-supplied in many

markets across the U.S., generating a favorable demand/supply balance

for owners. By contrast, fundamentals of traditional multifamily

apartments in many markets are out of balance due to slowing demand and

elevated supply over the next two years.

Senior Housing Market Forecast

The senior housing sector continues its strong post-COVID recovery,

evidenced by continued occupancy gains and rental growth momentum. New

supply continues to remain muted given high construction costs and lack

of affordable construction financing. Additionally, labor cost growth is

slowing from elevated levels, contributing to widening margins and

attractive growth in net operating income.

The accelerating growth in the 70- to 85-year-old group, plus the wealth accumulated over recent years, should continue to drive strong demand for senior housing facilities. Helped by appreciation in equities and housing, affordability metrics have improved by more than 10 percentage points over the past decade, enough to pay six years of care (three times the average length of stay), a significant rise from four-and-a-half years of care in 2013.5

As a result of the demand/supply mismatch, occupancy has increased in the top 50 markets from 80% in 2021 to 85% today, which still trails the pre-COVID average of 89%.6 Over the same period, rents have increased by 13 percent.7

Potential Opportunities

We believe the current macroeconomic uncertainty and the

dislocation in the capital markets is creating opportunities to acquire

senior housing assets at an increasingly attractive basis (20% below

replacement cost) and yield profile (200bps+ above implied public market

pricing). The combination of financial stress and fatigue faced by

owners during COVID, inflation challenges (wages, food, supplies),

spiking interest rates, and a highly fragmented ownership base, is

likely to offer attractive investment opportunities.

While the fundamentals and investment thesis for senior housing are compelling, the subtleties of different care segments and the service-oriented nature of caring for elderly residents create operational risk, requiring a nuanced investment strategy and dedicated operating expertise.

Conclusion

Aging populations impact all real estate sectors. As individuals get

older, they leave the workforce, potentially reducing office demand.

They spend more on healthcare and travel and less on consumer goods,

potentially impacting hotel and retail demand. They also change their

living preferences, moving from apartments to single-family homes to

senior living facilities across different acuity spectrums. While

pervasive across all sectors, we believe that single-family rentals and

senior housing will be the biggest beneficiaries.

Diesen Beitrag teilen: