Henderson: Eurozone economy solid - money trends stable

The Eurozone economy performed solidly in 2016

05.01.2017 | 10:40 Uhr

GDP rose by 1.7% in the year to the third quarter, equal to growth in the US and well above “potential” expansion estimated by the EU Commission at only 1.0% in 2016. Domestic demand increased by 1.9%. Available evidence suggests a similar pace of growth in the fourth quarter, while the OECD’s Eurozone leading indicator has strengthened.

GDP expansion was above potential in 2016 for the third successive year. Accordingly, the unemployment rate has fallen steadily from a 2013 peak of 12.1% to 9.8% in October 2016. The decline of 0.8 percentage points (pp) over the latest 12 months compares with drops of 0.4 pp in the US, 0.2 pp in Japan and 0.4 pp in the UK.

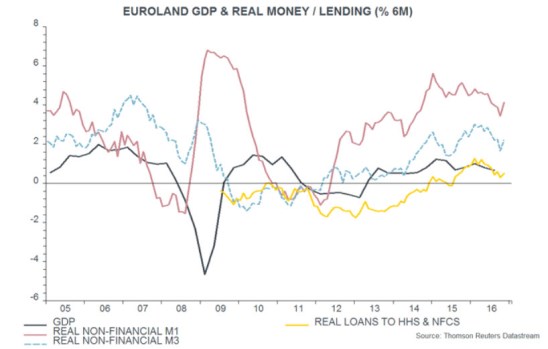

Monetary trends suggest that respectable growth will continue. Narrow and broad money rose strongly in November, reversing October softness. The preferred measure for economic forecasting purposes here is the six-month growth rate of real (i.e. consumer price inflation-adjusted) non-financial M1, comprising holdings of currency and overnight deposits by households and non-financial corporations. This rebounded to a four-month high in November and is robust by historical standards – see first chart.

Will the ECB’s decision to reduce QE securities purchases from €80 billion per month to €60 billion from April 2017 have a negative impact on monetary trends? Probably not. As previously discussed, the boost to broad money from QE has been more than offset an outflow of capital from the region – “excess” liquidity, in other words, appears to have been exported, pushing down the euro, rather than feeding through to stronger domestic demand. The view here is that solid economic performance reflects falling interest rates and an easing of fiscal austerity, with QE of little import.

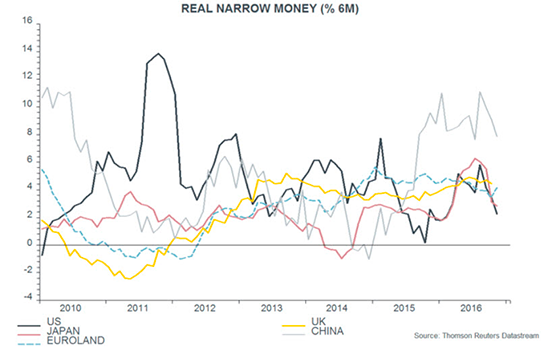

The planned reduction in QE may curb excess liquidity creation and slow capital outflows, with the extent of any decline dependent partly on political developments. The current account surplus, meanwhile, remains strong – €344 billion in the 12 months to October, equivalent to 3.2% of GDP. Six-month real narrow money growth is higher in the Eurozone than in the US and Japan, though lower than in China – second chart. The Eurozone / US gap casts doubt on the consensus view that US relative economic strength will drive a further widening of interest rate differentials in favour of the US dollar during 2017.

Die Wertentwicklung in der Vergangenheit ist kein zuverlässiger Indikator für die künftige Wertentwicklung. Alle Performance-Angaben beinhalten Erträge und Kapitalgewinne bzw. -verluste, aber keine wiederkehrenden Gebühren oder sonstigen Ausgaben des Fond.

Die Informationen in diesem Artikel stellen keine Anlageberatung dar.

Diesen Beitrag teilen: