Henderson: Multi-Asset Outlook 2017: More, more, more! – Growth, inflation, politics

Paul O’Connor, Head of Multi-Asset, reviews 2016’s lessons, and details the key themes that investors should prepare for in 2017. He explains which areas of the market look most and least appealing from a cross-asset perspective.

09.01.2017 | 11:01 Uhr

What lessons have you learned from 2016?

One key lesson is that investors can no longer rely on successive waves of central bank policy support to keep driving markets higher. The great monetary easing is over. In our view this implies that many of the trends that drove strong asset returns in the post-crisis years, such as the decline in bond yields, the rise in equity valuations, and the compression of credit spreads, are now close to exhaustion. This doesn’t mean that investors can’t make money in 2017, but it does suggest that returns will be lower and more varied than in recent years. Asset allocation and active management will be more important than ever.

The second key lesson from 2016 is that politics is returning as a major influence on financial markets after more than three decades during which its impact was supressed by globalisation, deregulation, and increasingly free markets. While the market-jolting political events of the last year – most notably ‘Brexit’ and the US presidential election – had their origins in domestic political dynamics, they also reflect a seismic shift in global politics that looks set to reverberate further around the world in 2017 and beyond. Politics is back. This is a regime change.

Themes for 2017: more growth, more inflation, more politics

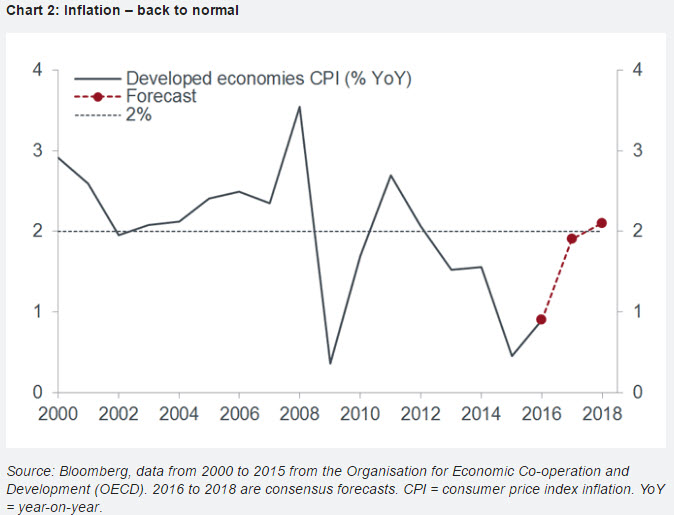

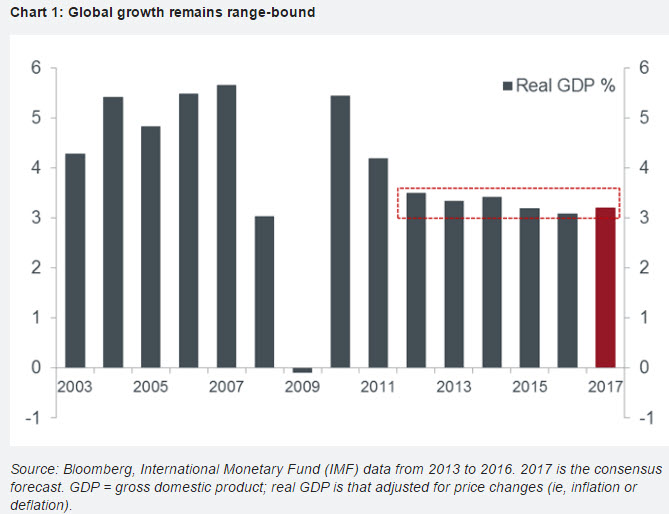

The global economy looks set to continue its steady post-crisis recovery in 2017, with real growth remaining in the 3-3.5% range for the sixth consecutive year. The good news is that the recovery is broadening, with all of the 20 largest economies expected to grow for the first time since 2010. Still, in Europe and the US, political developments add an unusually high level of uncertainty to the outlook. In the emerging world, China is the wildcard. Although Chinese growth remained resilient in 2016, the threats of a financial accident or a significant loss of macro momentum will be hard to dispel until structural tensions have eased. That will probably be a multi-year story.

While the trend in global growth remains fairly steady, inflation in the major economies is making a v-shaped rebound. Consensus forecasts predict that inflation in the developed economies should reach 2% this year for the first time since 2012. A key reason for the improving outlook is the stabilisation of commodity prices, which have been depressing headline inflation (which includes food and energy) for the last couple of years. The return of inflation to more normal levels in 2017 will boost nominal growth (that unadjusted for inflation) and corporate earnings. It may also erode support for the ‘secular stagnation’ (prolonged slow growth) narrative that has been widely embraced of late. Furthermore, while underlying inflation remains subdued in the eurozone and Japan, wages and prices are recovering more broadly in the US, which means that any further inflation surprises there will probably put upwards pressure on interest rate expectations.

A new era of elevated political risk

Most of the current generation of investors have been exposed to significant market setbacks resulting from economic and financial crises during their careers, but few will have experienced anything like the politically-driven market turbulence of 2016. Unfortunately, the balance of evidence suggests that last year’s events mark the beginning of a new era of elevated political risk. Event risk is high in 2017 – if things go badly we might well find ourselves in the most volatile political risk environment for decades. The known unknowns for this year are: the new US administration, ‘Brexit’ negotiations, and elections in France, Germany, and possibly Italy. Beyond these, a number of more general and potentially troubling political dynamics are evolving in the developed world. Forces such as the rise in populism and nationalism and a backlash against globalisation are prompting growing support for protectionist policy and immigration controls. In the emerging world, uncertainty surrounding China’s future relationship with the US, Russia’s strategic ambitions, and the ever-fragile state of the Middle East all loom over the medium-term outlook.

With regards to ‘Brexit’, the initial focus will be on whether the courts will impede the government’s desire to trigger Article 50 in during the first quarter of the year. Delays are certainly possible. Beyond this, lies the major question of how the government will prioritise conflicting objectives in the negotiations. While domestic political pressures argue for a fast, clean Brexit prioritising immigration-control, economic stability considerations argue for a focus on single-market access and a transitional arrangement to smooth the European Union (EU) exit. Of course, the UK’s stance is only the start of the negotiation process – the ultimate outcome will be largely determined by whatever new relationship the EU offers up. This will probably only emerge after the UK has triggered Article 50 and is likely to be forged in a blaze of threats, recriminations, and brinkmanship. It seems highly probable that market concerns about the political or economic implications of Brexit will flare up significantly again at some stage in 2017.

On balance, the big picture is one of an ongoing global recovery that will face the persistent threat of being derailed by politics. Still, while we do seem to have moved into a world in which previously unimaginable geopolitical outcomes are now conceivable, it is far from inevitable that the worst case scenarios will materialise, nor is it obvious that politics will overwhelm the recovery. Even 2016’s political eruptions did not have a lasting impact on economic growth. Indeed, one growth-positive theme worth noting is that governments tend to ease fiscal policy when anti-establishment movements gather momentum. This has already begun to happen in the UK and parts of Europe and will materialise more dramatically in the US soon, if Donald Trump gets his way.

Our multi-asset positioning: favouring cyclical assets

The combination of strengthening global growth, diminishing central bank support, and an unusually wide range of potential political outcomes is certainly a challenging backdrop for asset allocation. While our central view remains that the global recovery can withstand the anticipated political turbulence, we will continue to favour assets that can benefit from stronger growth and are resilient to the withdrawal of central bank liquidity. Accordingly, equities remains our favourite asset class, we are neutral on credit and remain wary of government bonds.

In equities, we start the year well-diversified across the major markets. While most of the policies expected from the Trump government look encouraging for US stocks, this appears well priced in. Eurozone and Japanese equities have their own attractions, being cyclical markets that typically perform well when global growth is picking up and bond yields are rising. We reduced our emerging market equity exposure back to neutral in the fourth quarter of 2016, reflecting concerns about the potential impact of some of the policy ideas being associated with the new US administration. Although the improving tone in commodities is supportive for emerging market assets, we need to feel more comfortable about the policy intentions of the Trump administration before rebuilding strategic positions here.

Where fixed income markets are concerned, we do not believe that the adjustment to the changing macroeconomic and policy environment is yet complete. We see scope for higher interest rate expectations in the US as well as higher real yields and term premia* in government bond markets globally. If we are right on this, then 2017 could see a fairly significant rotation out of bond funds into equities. It’s worth recalling that global bond funds have enjoyed US$1.5tn net inflows over the past decade, while equites in aggregate have received nothing at all.

Opportunities for dynamic asset allocation

Of course, as discussed above, we see multiple political developments that could disrupt confidence in the economic recovery and raise questions about our base case view. Beyond the politics, with asset valuations generally looking quite high, markets will remain sensitive to any reappraisal of either the growth or policy outlook. While growth disappointments could undermine confidence in reflation trades** – positive growth surprises could worry bond markets. At the very least, we expect occasional market setbacks and frantic changes in market leadership when political or economic concerns do flare up. This is an environment which should provide plenty of opportunities for dynamic asset allocation and active management more generally. While many active managers have struggled to outperform benchmarks in the high-return, liquidity-driven markets of recent years, the lower return, more fundamentally-driven regime that we anticipate is the sort of environment in which we expect them to add value.

So, although our core view of the world argues for a reflationary tilt to our portfolios, we are not “all in” on this theme and are taking a more balanced, diversified approach. In particular, alternative asset classes with low correlations to traditional markets, such as CTAs***, commodities, and absolute return funds have a major role to play in this sort of environment.

* Term premium = the additional compensation investors demand to hold a longer-term bond relative to a series of shorter-term bonds.

** Trading that reflects a belief in a reflationary backdrop, where prices rise alongside growth and inflation. Reflationary policies, such as reducing taxes and lowering interest rates, are designed to expand a country's output and curb the effects of deflation.

***Commodity trading advisors’ funds which deal in futures contracts, commodity options and/or swaps.

Die Wertentwicklung in der Vergangenheit ist kein zuverlässiger Indikator für die künftige Wertentwicklung. Alle Performance-Angaben beinhalten Erträge und Kapitalgewinne bzw. -verluste, aber keine wiederkehrenden Gebühren oder sonstigen Ausgaben des Fond.

Die Informationen in diesem Artikel stellen keine Anlageberatung dar.

Diesen Beitrag teilen: