Schroders: Eurozone − Political risk still simmering

Though many of Europe’s major political obstacles have been overcome, events in Spain highlight that political risk continues to simmer under the surface. These risks are contained for now, helped by quantitative easing which is set to continue into 2018.

10.11.2017 | 10:10 Uhr

The major political obstacles, which had held back European risk assets, have now been overcome. However, events in Austria, Spain and Italy highlight the ongoing trend towards populist, nationalist and now regionalist sentiment.

In Austria, although the far right Freedom Party (FPÖ) was recently defeated in elections for the legislative parliament, it could enter government as part of a right wing coalition.

In Spain, the Catalan referendum does not change the status quo in Spain. The referendum was deemed illegal by the constitutional court beforehand, and the low turn-out calls into questions the validity of the vote itself.

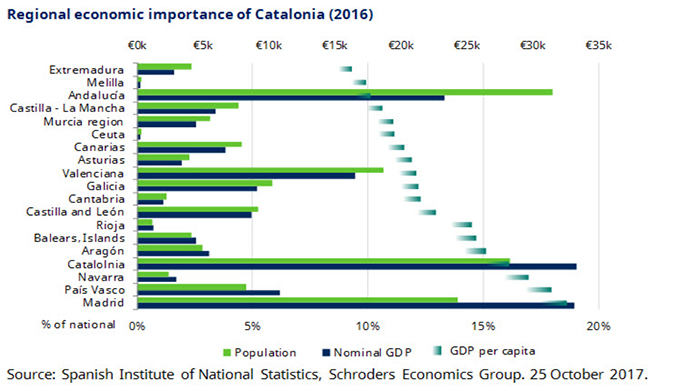

The loss of Catalonia to Spain would be significant. In 2016, Catalonia was the largest economic region with 19% of Spanish GDP, and the second most populated with 16.2% of the overall population. It is the fourth richest region using GDP per capita, and its main industries are tourism, food and chemicals manufacturing.

Catalonia is also important as it makes a considerable contribution to the Spain’s public finances. In absolute terms, Catalonia made a net contribution of €9.9 billion in 2014 (latest data), which was worth 4.8% of its GDP. This is significantly smaller than the net contribution made by Madrid, but is still very important – making up 30.5% of the overall budget.

We do not expect the Catalans to achieve independence, at least not without the consent of the rest of Spain, but in the meantime, the uncertainty of the potential break-away for the Catalan region could dampen growth.

This month also saw referendums in Lombardy and Veneto in Italy where voters backed reforms to grant the regions greater autonomy. Although these referendums had nothing to do with separatism today, they may set the path for such a course in the future. After all, this is how Spain's mess started.

Political risk continues to simmer under the surface as highlighted by these events, but such risks should be contained and have a limited impact on markets.

Upbeat ECB to extend QE into 2018

Meanwhile, the eurozone economy continues to perform strongly, while the European Central Bank’s (ECB) quantitative easing (QE) acts as a veil, covering up many of the monetary union's problems and fragilities.

But the QE veil is about to be withdrawn. At the October press conference, ECB president Mario Draghi confirmed the decision to keep interest rates unchanged and to extend QE to September 2018, but also to reduce purchases from the current pace of €60 billion per month to €30 billion per month.

While he gave a positive assessment of the eurozone economic outlook, the inflationary picture is more uncertain. As a result, the ECB’s view is that stimulus should continue, but should be scaled back.

We expect the ECB to probably extend QE again at the end of next year to finally end the programme in December 2018, paving the way for a rise in interest rates in the first half of 2019.

In the meantime, this environment of strong growth, low inflation and ample liquidity should help support the outperformance of European equities.

Die hierin geäußerten Ansichten und Meinungen stellen nicht notwendigerweise die in anderen Mitteilungen, Strategien oder Fonds von Schroders oder anderen Marktteilnehmern ausgedrückten oder aufgeführten Ansichten dar.

Der Beitrag wurde am 07.11.17 auch auf schroders.com veröffentlicht.

Diesen Beitrag teilen: