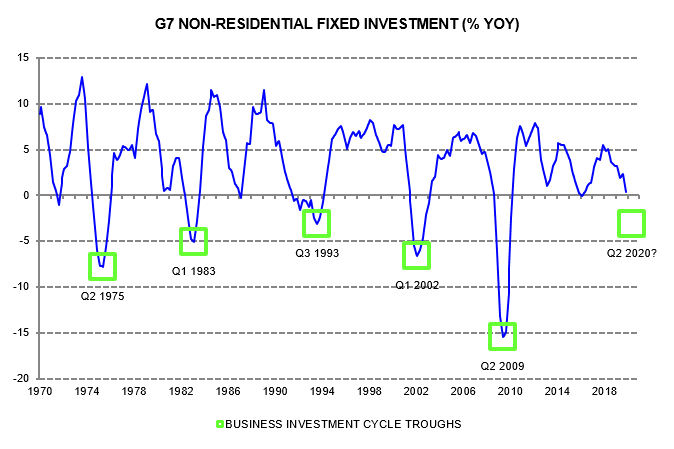

The business investment or Juglar cycle (after nineteenth century French

economist Clément Juglar) ranges between 7 and 11 years. Cycle lengths

are measured between troughs. Lows are marked by a year-on-year

contraction in investment. The last G7 trough occurred in Q2 2009 and

ended a short cycle (7.25 years) – see first chart. This suggested that

the current cycle would be of above-average length – the 11 year maximum

would imply a trough in Q2 2020.

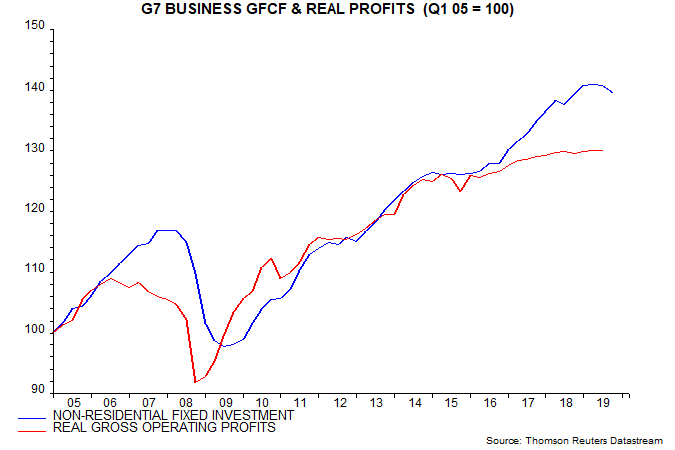

Previous posts noted that G7 business investment had slowed but was

still rising year-on-year as of Q3 2019. Growth since 2016 had opened up

a large gap with stagnant real gross operating profits – second chart.

This suggested that investment would weaken into H1 2020 – contrary to a

consensus expectation that the US / China trade “truce” would trigger a

rebound.

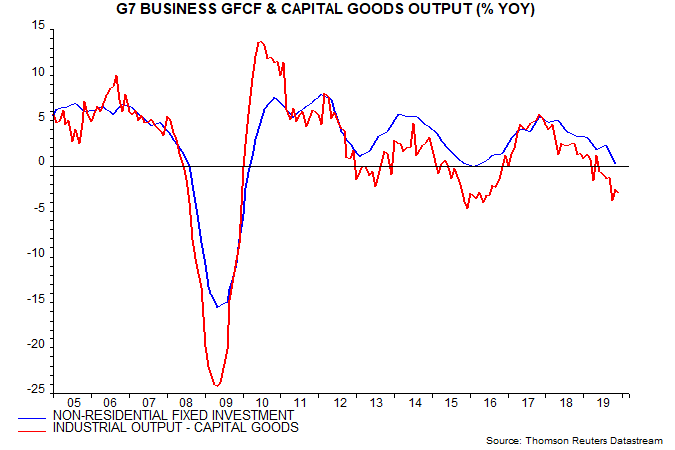

The G7 year-on-year investment change is estimated to have fallen to

around zero in Q4 2019, with weakness confirmed by declining industrial

output of capital goods – third chart.

The

year-on-year investment change also reached zero in Q1 2016, with

capital goods output falling. The possibility that the business

investment cycle had reached a trough was considered here but rejected

because 1) the year-on-year change had not turned negative, 2) the

implied cycle length of 6.75 years was outside the 7 to 11 year range

and 3) weakness was energy-focused, following the 2014-15 oil price

collapse, rather than general.

The year-on-year investment change was expected to turn negative in

H1 2020 even before the coronavirus shock, partly reflecting an

unfavourable base effect – investment rose by 1.1% between Q4 2018 and

Q2 2019. The shock will magnify the fall and may push back the trough to

Q2 2020.

What reasons are there to expect business investment to recover in H2

2020, apart from the time limit on weakness implied by the 11 year

maximum cycle length? The fall in long-term interest rates since late

2018 is stimulating housing activity and should start to support

business investment – which usually responds with a longer lag – later

in 2020. Business real narrow money trends, meanwhile, anticipate

turning points in the investment cycle and recovered in the US, Japan

and Euroland during 2019.

Diesen Beitrag teilen: